Attachment: Notes from meeting with Steve Eagle, finance director of the CS Group

Acquisition of Canary Co

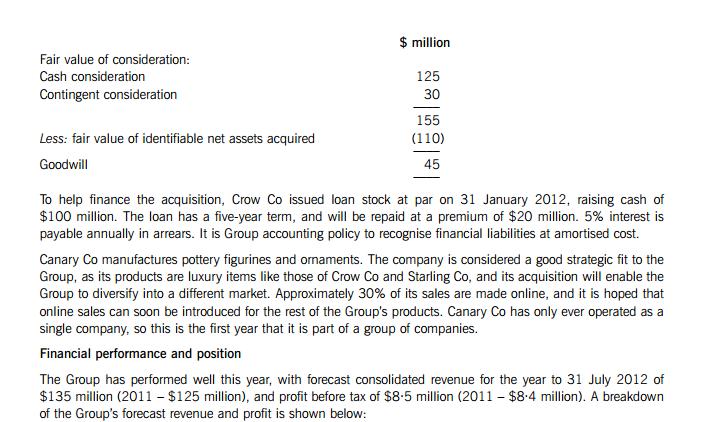

The most significant event for the CS Group this year was the acquisition of Canary Co, which took place on

1 February 2012. Crow Co purchased all of Canary Co’s equity shares for cash consideration of $125 million,

and further contingent consideration of $30 million will be paid on the third anniversary of the acquisition, if the

Group’s revenue grows by at least 8% per annum. Crow Co engaged an external provider to perform due diligence

on Canary Co, whose report indicated that the fair value of Canary Co’s net assets was estimated to be

$110 million at the date of acquisition. Goodwill arising on the acquisition has been calculated as follows:

Section B TWO questions ONLY to be attempted

3 (a) You are a manager in Lark & Co, responsible for the audit of Heron Co, an owner-managed business which

operates a chain of bars and restaurants. This is your firm’s first year auditing the client and the audit for the year

ended 31 March 2012 is underway. The audit senior sends a note for your attention:

‘When I was auditing revenue I noticed something strange. Heron Co’s revenue, which is almost entirely

cash-based, is recognised at $55 million in the draft financial statements. However, the accounting system

shows that till receipts for cash paid by customers amount to only $35 million. This seemed odd, so I questioned

Ava Gull, the financial controller about this. She said that Jack Heron, the company’s owner, deals with cash

receipts and posts through journals dealing with cash and revenue. Ava asked Jack the reason for these journals

but he refused to give an explanation.

‘While auditing cash, I noticed a payment of $2 million made by electronic transfer from the company’s bank

account to an overseas financial institution. The bank statement showed that the transfer was authorised by Jack

Heron, but no other documentation regarding the transfer was available.

‘Alarmed by the size of this transaction, and the lack of evidence to support it, I questioned Jack Heron, asking

him about the source of cash receipts and the reason for electronic transfer. He would not give any answers and

became quite aggressive.’

Required:

(i) Discuss the implications of the circumstances described in the audit senior’s note; and (6 marks)

(ii) Explain the nature of any reporting that should take place by the audit senior. (3 marks)

(b) You are also responsible for the audit of Coot Co, and you are currently reviewing the working papers of the audit

for the year ended 28 February 2012. In the working papers dealing with payroll, the audit junior has

commented as follows:

‘Several new employees have been added to the company’s payroll during the year, with combined payments of

$125,000 being made to them. There does not appear to be any authorisation for these additions. When I

questioned the payroll supervisor who made the amendments, she said that no authorisation was needed

because the new employees are only working for the company on a temporary basis. However, when discussing

staffing levels with management, it was stated that no new employees have been taken on this year. Other than

the tests of controls planned, no other audit work has been performed.’

Required:

In relation to the audit of Coot Co’s payroll:

Explain the meaning of the term ‘professional skepticism’, and recommend any further actions that should

be taken by the auditor. (6 marks)

(15 marks)

84 You are a senior manager in the audit department of Raven & Co. You are reviewing two situations which have arisen

in respect of audit clients, which were recently discussed at the monthly audit managers’ meeting:

Grouse Co is a significant audit client which develops software packages. Its managing director, Max Partridge, has

contacted one of your firm’s partners regarding a potential business opportunity. The proposal is that Grouse Co and

Raven & Co could jointly develop accounting and tax calculation software, and that revenue from sales of the software

would be equally split between the two firms. Max thinks that Raven & Co’s audit clients would be a good customer

base for the product.

Plover Co is a private hospital which provides elective medical services, such as laser eye surgery to improve eyesight.

The audit of its financial statements for the year ended 31 March 2012 is currently taking place. The audit senior

overheard one of the surgeons who performs laser surgery saying to his colleague that he is hoping to finish his

medical qualification soon, and that he was glad that Plover Co did not check his references before employing him.

While completing the subsequent events audit procedures, the audit senior found a letter from a patient’s solicitor

claiming compensation from Plover Co in relation to alleged medical negligence resulting in injury to the patient.

Required:

Identify and discuss the ethical, commercial and other professional issues raised, and recommend any actions

that should be taken in respect of:

(a) Grouse Co; (8 marks)

(b) Plover Co. (7 marks)

(15 marks)

9 [P.T.O.5 You are the partner responsible for performing an engagement quality control review on the audit of Snipe Co. You

are currently reviewing the audit working papers and draft audit report on the financial statements of Snipe Co for the

year ended 31 January 2012. The draft financial statements recognise revenue of $85 million, profit before tax of

$1 million, and total assets of $175 million.

(a) During the year Snipe Co’s factory was extended by the self-construction of a new processing area, at a total cost

of $5 million. Included in the costs capitalised are borrowing costs of $100,000, incurred during the six-month

period of construction. A loan of $4 million carrying an interest rate of 5% was taken out in respect of the

construction on 1 March 2011, when construction started. The new processing area was ready for use on

1 September 2011, and began to be used on 1 December 2011. Its estimated useful life is 15 years.

Required:

In respect of your file review of non-current assets:

Comment on the matters that should be considered, and the evidence you would expect to find regarding the

new processing area. (8 marks)

(b) Snipe Co has in place a defined benefit pension plan for its employees. An actuarial valuation on 31 January

2012 indicated that the plan is in deficit by $105 million. The deficit is not recognised in the statement of

financial position. An extract from the draft audit report is given below:

Auditor’s opinion

In our opinion, because of the significance of the matter discussed below, the financial statements do not give a

true and fair view of the financial position of Snipe Co as at 31 January 2012, and of its financial performance

and cash flows for the year then ended in accordance with Hong Kong Financial Reporting Standards.

Explanation of adverse opinion in relation to pension

The financial statements do not include the company’s pension plan. This deliberate omission contravenes

accepted accounting practice and means that the accounts are not properly prepared.

Required:

Critically appraise the extract from the proposed audit report of Snipe Co for the year ended 31 January

2012.

Note: you are NOT required to re-draft the extract of the audit report. (7 marks)

(15 marks)

End of Question Paper

It will take time to gain this knowledge and to properly document it. Given that the company’s year end is less than one

month away, it is important that we plan to begin this work as soon as possible, to avoid any delay to the audit of either

the individual or the consolidated financial statements. We need to arrange with the client for members of the audit team

to have access to the necessary information, including the accounting system, and to hold the necessary discussions

with management. Once we have gained a thorough understanding of Canary Co we will be in a position to develop an

audit strategy and detailed audit plan.

We have been provided with the CS Group’s forecast revenue and profit for the year, but need to perform a detailed

preliminary analytical review on a full set of Canary Co’s financial statements to fully understand the financial

performance and position of the company, and to begin to form a view on materiality. This review will also highlight any

significant transactions that have occurred this year.

As this is an initial audit engagement, we are required by HKSA 300 Planning an Audit of Financial Statements to

communicate with the predecessor auditor. If this has not yet occurred, we should contact the predecessor auditor and

enquire regarding matters which may influence our audit strategy and plan. We may request access to their working

papers, especially in respect of any matters which appear contentious or significant. We should also review the prior

year audit opinion as this may include matters that impact on this year’s audit.

As the opening balances were audited by another firm, we should plan to perform additional work on opening balances

as required by HKSA 510 Initial Audit Engagements Opening Balances.

Consolidated financial statements audit

As Canary Co will form a component of the consolidated financial statements on which we are required to form an

opinion, we must also consider the implications of its acquisition for the audit of the CS Group accounts. HKSA 600

Special Considerations Audits of Group Financial Statements (Including the Work of Component Auditors) requires

that the group auditor must identify whether components of the group are significant components. Based on the forecast

results Canary Co is a significant component, as it represents 119% of forecast consolidated revenue, and 235% of

forecast consolidated profit before tax.

As our firm is auditing the individual financial statements of Canary Co, our risk assessment and planned response to

risks identified at individual company level will also be relevant to the audit of the consolidated financial statements.

However, we must also plan to obtain audit evidence in respect of balances and transactions which only become relevant

on consolidation, such as any inter-company transactions that may occur.

A significant matter which must be addressed is that of the different financial year end of Canary Co. We will have

audited Canary Co’s figures to its year end of 30 June 2012, but an additional month will be consolidated to bring the

accounts into line with the 31 July year end of the rest of the CS Group. Therefore, additional procedures will have to

be planned to gain audit evidence on significant events and transactions of Canary Co which occur in July 2012. This

may not entail much extra work, as we will be conducting a review of subsequent events anyway, as part of our audit

of the individual financial statements.

It may be that Canary Co’s year end will be changed to bring into line with the rest of the CS Group. If so, we need to

obtain copies of the documentary evidence to demonstrate that this has been done.14

When performing analytical procedures on the consolidated financial statements, we must be careful that when

comparing this year’s results with prior periods, we are making reasonable comparisons. This is because Canary Co’s

results are only included since the date of acquisition on 1 February 2012 and comparative figures are not restated.

Calculations such as return on capital employed will also be distorted, as the consolidated statement of financial position

at 31 July 2012 includes Canary Co’s assets and liabilities in full, but the consolidated income statement will only

include six months’ profit generated from those assets.

Materiality needs to be assessed based on the new, enlarged group structure. Materiality for the group financial

statements as a whole shall be determined when establishing the overall group audit strategy. The addition of Canary

Co to the group during the year is likely to cause materiality to be different from previous years, possibly affecting audit

strategy and the extent of testing in some areas.

Finally, we must ensure that sufficient time and resource is allocated to the audit of the consolidated financial statements

as there will be additional work to perform on auditing the acquisition itself, including the goodwill asset, the fair value

of assets acquired, the cash outflows, the contingent consideration, and the notes to the financial statements. As this is

a complex area we should consider allocating this work to a senior, experienced member of the audit team. Relevant

financial statement risks and audit procedures in respect of goodwill are discussed later in these notes.

(ii) Risks of material misstatement

General matters

HKSA 315 provides examples of conditions and events that may indicate risks of material misstatement. These include

changes to corporate structure such as large acquisitions, moving into new lines of business and the installation of

significant new IT systems related to financial reporting. The CS Group has been involved in all three of these during

the financial year, so the audit generally should be approached as high risk.

Goodwill

The client has determined goodwill arising on the acquisition of Canary Co to be $45 million, which is material to the

consolidated financial statements, representing 82% of total assets. The various components of goodwill have specific

risks attached. For the consideration, the contingent element of the consideration is inherently risky, as its measurement

involves a judgement as to the probability of the amount being paid.

Currently, the full amount of contingent consideration is recognised, indicating that the amount is certain to be paid.

HKFRS 3 (Revised) Business Combinations requires that contingent consideration is recognised at fair value at the time

of the business combination, meaning that the probability of payment should be used in measuring the amount of

consideration that is recognised at acquisition. This part of the consideration could therefore be overstated, if the

assessment of probability of payment is incorrect.

Another risk is that the contingent consideration does not appear to have been discounted to present value as required

by HKFRS 3, again indicating that it is overstated.

The same risk factors apply to the individual financial statements of Crow Co, in which the cost of investment is

recognised as a non-current asset.

The other component of the goodwill calculation is the value of identifiable assets acquired, which HKFRS 3 requires to

be measured at fair value at the date of acquisition. This again is inherently risky, as estimating fair value can involve

uncertainty. Possibly the risk is reduced somewhat as the fair values have been determined by an external firm.

Goodwill should be tested for impairment annually according to HKAS 36 Impairment of Assets, and a test should be

performed in the year of acquisition, regardless of whether indicators of impairment exist. There is therefore a risk that

goodwill may be overstated if management has not conducted an impairment test at the year end. If the impairment

review were to indicate that goodwill is overstated, there would be implications for the cost of investment recognised in

Crow Co’s financial statements, which may also be overstated.

Loan stock

Crow Co has issued loan stock for $100 million, representing 182% of total assets, therefore this is material to the

consolidated financial statements. The loan will be repaid at a significant premium of $20 million, which should be

recognised as finance cost over the period of the loan using the amortised cost measurement method according to

HKFRS 9 Financial Instruments. A risk of misstatement arises if the premium relating to this financial year has not been

included in finance costs.

In addition, finance costs could be understated if interest payable has not been accrued. The loan carries 5% interest

per annum, and six months should be accrued by the 31 July year end, amounting to $25 million. Financial liabilities

and finance costs will be understated if this has not been accrued.

There is also a risk of inadequate disclosure regarding the loan in the notes to the financial statements. HKFRS 7

Financial Instruments: Disclosures requires narrative and numerical disclosures relating to financial instruments that give

rise to risk exposure. Given the materiality of the loan, it is likely that disclosure would be required.

The risks described above are relevant to Crow Co’s individual financial statements as well as the consolidated financial

statements.15

Online sales

There is a risk that revenue is not recognised at the correct time, as it can be difficult to establish with online sales when

the revenue recognition criteria of HKAS 18 Revenue have been met. This could mean that revenue and profits are at

risk of over or understatement. This is a significant issue as 30% of Canary Co’s sales are made online, which

approximates to sales of $48 million or 36% of this year’s consolidated revenue, and will be a higher percentage of

total sales next year when a full year of Canary Co’s revenue is consolidated.

Prior to the acquisition of Canary Co, the CS Group had no experience of online sales, which means that there will not

yet be a group accounting policy for online revenue recognition.

There may also be risks arising from the system not operating effectively or that controls are deficient leading to

inaccurate recording of sales.

Canary Co management

As this is the first time that Canary Co’s management will be involved with group financial reporting, they will be

unfamiliar with the processes used and information required by the CS Group in preparing the consolidated financial

statements. There is a risk that information provided may be inaccurate or incomplete, for example in relation to

inter-company transactions.

Financial performance

Looking at the consolidated revenue and profit figures, it appears that the group’s results are encouraging, with an

increase in revenue of 8% and in profit before tax of 12%.

The analysis reveals that Crow Co and Starling Co combined have a significantly reduced profit for the year, with revenue

also slightly reduced. The apparent increase in costs may be caused by one-off costs to do with the acquisition of Canary

Co, such as due diligence and legal costs. However there remains a risk of misstatement as costs could be overstated

or revenue understated.

Possible manipulation of financial statements

A risk of misstatement arises in relation to Canary Co as its financial statements have been prone to manipulation. In

particular, its management may have felt pressure to overstate revenue and profits in order to secure a good sale price

for the company. The existence of contingent consideration relating to the Group’s post acquisition revenue is also a

contributing factor to possible manipulation, as the Group will want to avoid paying the additional consideration.

Grant received

Starling Co has received a grant of $35 million in respect of environmentally friendly capital expenditure, of which

$25 million has already been spent. There is a risk in the recognition of the grant received. According to HKAS 20

Accounting for Government Grants and Disclosure of Government Assistance government grants shall be recognised as

income over the periods necessary to match them with the related costs which they are intended to compensate. This

means that the $35 million should not be recognised as income on receipt, but the income deferred and released to

profit over the estimated useful life of the assets to which it relates. There is a risk that an inappropriate amount has

been credited to profit this year.

A further risk arises in respect of the $10 million grant which has not yet been spent. Depending on the conditions of

the grant, some or all of it may become repayable if it is not spent on qualifying assets within a certain time, and a

provision may need to be recognised. $10 million represents 18% of consolidated assets, likely to be material to the

CS Group financial statements. It is likely to form a much greater percentage of Starling Co’s individual assets and

therefore be more material in its individual financial statements.

New IT system

A new system relevant to financial reporting was introduced to Crow Co and Starling Co. HKSA 315 indicates that the

installation of significant new IT systems related to financial reporting is an event that may indicate a risk of material

misstatement. Errors may have occurred in transferring data from the old to the new system, and the controls over the

new system may not be operating effectively.

Further, if Canary Co is not using the same IT system, there may be problems in performing its consolidation into the

CS Group, for example, in reconciling inter-company balances.16

Starling Co finance director

One of the subsidiaries currently lacks a finance director. This means that there may be a lack of personnel with

appropriate financial reporting and accounting skills, increasing the likelihood of error in Starling Co’s individual financial

statements, and meaning that inputs to the consolidated financial statements are also at risk of error. In addition, the

reason for the finance director leaving should be ascertained, as it could indicate a risk of material misstatement, for

example, if there was a disagreement over accounting policies.

(iii) Audit procedures relating to goodwill

Obtain the legal purchase agreement and confirm the date of the acquisition as being the date that control of

Canary Co passed to Crow Co.

From the legal purchase agreement, confirm the consideration paid, and the details of the contingent consideration,

including its amount, date potentially payable, and the factors on which payment depends.

Confirm that Canary Co is wholly owned by Crow Co through a review of its register of shareholders, and by

agreement to legal documentation or by a Companies House search.

Agree the cash payment of $125 million to cash book and bank statements.

Review the board minutes for discussion regarding, and approval of, the purchase of Canary Co.

Obtain the due diligence report prepared by the external provider and confirm the estimated fair value of net assets

at acquisition.

Discuss with management the reason for providing for the full amount of contingent consideration, and obtain

written representation concerning the accounting treatment.

Ask management to recalculate the contingent consideration on a discounted basis, and confirm goodwill is

recognised on this basis in the consolidated financial statements.

Tutorial note: Procedures relating to impairment testing of the goodwill at the year end are not relevant to the

requirement, which asks for procedures relating to the goodwill initially recognised on acquisition.

(b) Ethical matters regarding the CS Group

Firstly, regarding the audit engagement partner attending board meetings, there is nothing to prohibit an auditor attending the

board meetings of an audit client. Indeed it is common practice for this to occur, and there may be times when the auditor

should attend in order to raise issues with management and/or those charged with governance pertaining to the audit.

However, the auditor attending the client’s board meeting must be careful that they take no part in any management decisions

made at the meeting. If matters not relevant to the audit are debated on which the auditor’s opinion is sought, the auditor

could be deemed to be involved with management decisions, or to be providing an additional service to the client which

potentially creates a threat to objectivity.

IFAC’s Code of Ethics for Professional Accountants and ACCA’s Code of Ethics and Conduct both advise that if an auditor

serves as a director or officer of an audit client, the self-review and self-interest threats created would be so significant that

no safeguards could reduce the threats to an acceptable level. Accordingly, no partner or employee shall serve as a director

or officer of an audit client. In summary, it is acceptable for the audit engagement partner to attend the board meetings, as

long as he is not involved with making management decisions, and if he is not appointed to the board.

The second matter relates to an audit manager being seconded to Starling Co in a role as finance director. IFAC’s Code refers

to this situation as a temporary staff assignment, and states that the lending of staff by a firm to an audit client may create a

self-review threat. Such assistance may be given, but only for a short period of time and the firm’s personnel shall not be

involved in providing non-assurance services or assuming management responsibilities.

It seems that in this case, the temporary staff assignment should not go ahead, as clearly the audit manager would be making

management decisions involving the preparation of Starling Co’s individual financial statements, and providing information

for the consolidated financial statements. It is not likely that any safeguard could reduce the self-review threat created to an

acceptable level.

Finally, our firm has been asked to help in the recruitment of a new finance director to Starling Co. IFAC’s Code states that

providing recruitment services to an audit client may create self-interest, familiarity or intimidation threats. The existence and

significance of any threat will depend on factors such as the nature of the requested assistance, and the role of the person to

be recruited.

The significance of any threat created shall be evaluated and safeguards applied when necessary to eliminate the threat or

reduce it to an acceptable level. In all cases, the firm shall not assume management responsibilities, including acting as a

negotiator on the client’s behalf, and the hiring decision shall be left to the client.

The firm may generally provide such services as reviewing the professional qualifications of a number of applicants and

providing advice on their suitability for the post. In addition, the firm may interview candidates and advise on a candidate’s

competence for financial accounting, administrative or control positions.

Therefore Magpie & Co may provide some assistance in the recruitment of the new finance director, but may wish to put

safeguards in place such as obtaining written acknowledgement from the client that the ultimate decision will be made by

them. 17

2 (a) (i) The terms of the engagement to review and report on Hawk Co’s business plan and forecast financial statements should

be agreed in an engagement letter, separate from the audit engagement letter. The following matters should be included

in the terms of agreement:

Management’s responsibilities

The terms of the engagement should set out management’s responsibilities for the preparation of the business plan and

forecast financial statements, including all assumptions used, and for providing the auditor with all relevant information

and source data used in developing the assumptions. This is to clarify the roles of management and of Lapwing & Co,

and reduce the scope for any misunderstanding.

The intended use of the business plan and report

It should be confirmed that the report will be provided to the bank and that it will not be distributed or made available

to other parties. This will establish the potential liability of Lapwing & Co to third parties, and help to determine the need

and extent of any liability disclaimer that may be considered necessary. Lapwing & Co should also establish that the

bank will use the report only in helping to reach a decision in respect of the additional finance being sought by

Hawk Co.

The elements of the business plan to be included in the review and report

The extent of the review should be agreed. Lapwing & Co need to determine whether they are being asked to report just

on the forecast financial statements, or on the whole business plan including any narrative descriptions or explanations

of Hawk Co’s intended future business activities. This will help to determine the scope of the work involved and its

complexity.

The period covered by the forecasts

This should be confirmed when agreeing the terms of the engagement, as assumptions become more speculative as the

length of the period covered increases, making it more difficult for Lapwing & Co to substantiate the acceptability of the

figures, and increasing the risk of the engagement. It should also be confirmed that a 12-month forecast period is

sufficient for the bank’s purposes.

The nature of the assumptions used in the business plan

It is crucial that Lapwing & Co determine the nature of assumptions, especially whether the assumptions are based on

best estimates or are hypothetical. This is important because ISAE 3400 The Examination of Prospective Financial

Information states that the auditor should not accept, or should withdraw from, an engagement when the assumptions

are clearly unrealistic or when the auditor believes that the prospective financial information will be inappropriate for its

intended use.

The planned contents of the assurance report

The engagement letter should confirm the planned elements of the report to be issued, to avoid any misunderstanding

with management. In particular, Lapwing & Co should clarify that their report will contain a statement of negative

assurance as to whether the assumptions provide a reasonable basis for the prospective financial information, and an

opinion as to whether the prospective financial information is properly prepared on the basis of the assumptions and is

presented in accordance with the relevant financial reporting framework. The bank may require the report to be in a

particular format and include specific wordings in order to make their lending decision.

Tutorial note: Credit will also be awarded for discussion of other matters relevant to agreeing the terms of the

engagement, such as confirming the fee and billing arrangements, and confirming the deadline for completion of the

engagement.

(ii) General procedures

Re-perform calculations to confirm the arithmetic accuracy of the forecast financial statements.

Agree the unaudited figures for the period to 31 May 2012 to management accounts, and agree the cash figure to

bank statement or bank reconciliation.

Confirm the consistency of the accounting policies used in the preparation of the forecast financial statements with

those used in the last audited financial statements.

Consider the accuracy of forecasts prepared in prior periods by comparison with actual results and discuss with

management the reasons for any significant variances.

Perform analytical procedures to assess the reasonableness of the forecast financial statements. For example,

finance charges should increase in line with the additional finance being sought.

Discuss the extent to which the joint venture with Kestrel Co has been included in the forecast financial statements.

Review any agreement with Kestrel Co, or minutes of meetings at which the joint venture has been discussed to

understand the nature, scale, and timeframe of the proposed joint business arrangement.

Review any projected financial information for the joint venture, and agree any components relating to it into the

forecast financial statements. 18

Forecast income statement

Consider the reasonableness of forecast trends in the light of auditor’s knowledge of Hawk Co’s business and the

current and forecast economic situation and any other relevant external factors.

Discuss the reason for the anticipated 214% increase in revenue with management, to understand if the increase

is due to the inclusion of figures relating to the joint venture with Kestrel Co, or other factors.

Discuss the trend in operating profit with management the operating margin is forecast to improve from 30% to

338%. This improvement may be due to the sale of the underperforming Beak Retail park.

Obtain a breakdown of items included in forecast operating expenses and perform an analytical review to compare

to those included in the 2012 figures, to check for any omissions.

Using the cost breakdown, consider whether depreciation charges have increased in line with the planned capital

expenditure.

Request confirmation from the bank of the potential terms of the $30 million loan being negotiated, to confirm the

interest rate at 4%. Consider whether the finance charge in the forecast income statement appears reasonable. (If

the loan is advanced in August, it should increase the company’s finance charge by $1 million ($30 million x 4%

x 10/12).)

Discuss the potential sale of Beak Retail with management and review relevant board minutes, to obtain

understanding of the likelihood of the sale, and the main terms of the sale negotiation.

Recalculate the profit on the planned disposal, agreeing the potential proceeds to any written documentation

relating to the sale, vendor’s due diligence report, or draft legal documentation if available.

Agree the potential proceeds on disposal to management’s cash flow forecast, and confirm that operating cash

flows relevant to Beak Retail are not included from the anticipated date of its sale.

Discuss the reason for not including current tax in the profit forecast.

Forecast statement of financial position

Agree the increase in property, plant and equipment to an authorised capital expenditure budget, and to any plans

for the joint development with Kestrel Co.

Obtain and review a reconciliation of the movement in property, plant and equipment. Agree that all assets relating

to Beak Retail are derecognised on its disposal, and that any assets relating to the joint development with Kestrel

Co are recognised in accordance with capital expenditure forecasts, and are properly recognised per HKFRS 11

Joint Arrangements.

Discuss the planned increase in equity with management to understand the reason for any planned share issue,

its date and the nature of the share issue (rights issue or issue at full market price being the most likely).

Perform analytical procedures on working capital and discuss trends with management, for example, receivables

days is forecast to reduce from 58 to 53 days, and the reason for this should be obtained.

Tutorial note: Credit will be awarded for other examples of ratios calculated on the figures provided such as

inventory turnover and average payables payment period.

Agree the increase in long-term borrowings to documentation relating to the new loan, and also to the forecast cash

flow statement (where it should be included as a cash flow arising from financing activities).

Discuss the deferred tax provision with management to understand why no movement on the balance is forecast,

particularly given the planned capital expenditure.

Obtain and review a forecast statement of changes in equity to ensure that movements in retained earnings appear

reasonable. (Retained earnings are forecast to increase by $800,000, but the profit forecast for the period is

$1052 million there must be other items taken through retained earnings such as a planned dividend.)

Agree the movement in cash, and the forecast closing cash position to a cash flow forecast.

(b) Briefing notes

From: Audit manager

To: Audit partner

Regarding: Osprey Co

Introduction

These briefing notes will firstly recommend the principal audit procedures to be performed in respect of the costs of closure

of the factory involved in the environmental contamination. I will also discuss the difficulties in measuring and reporting on

environmental and social performance.

(i) Recommended audit procedures

Review board minutes for discussion of the closure and restructuring, noting the date the decision was made to

restructure, which should be before the year end.19

Obtain any detailed and formal plan relating to the closure of the factory and relocation of its operations, noting the

date the plan was approved, which should be before the year end.

Discuss with management any indication that the company has started to implement the plan prior to the year end,

e.g. the date of any public announcement, the date that plant began to be dismantled.

Physically inspect the factory for evidence that dismantling has commenced.

Tutorial note: The procedures outlined above should establish whether a constructive obligation exists at the year

end, in which case it is appropriate to recognise a provision according to HKAS 37 Provisions, Contingent

Liabilities and Contingent Assets. If there is no detailed formal plan in place, and no evidence that a valid

expectation exists that the company will carry out the restructuring at the year end, then no provision should be

recognised.

Obtain a breakdown of the $125 million costs of closure and review to ensure that only relevant costs have been

included, e.g. redundancy payments, lease cancellation fees. This is an important procedure for the potential

overstatement of the provision.

Cast the schedule for arithmetic accuracy.

Agree a sample of relevant costs included in the provision to supporting documentation, e.g. redundancy payments

to employees’ contracts, lease cancellation fees (if any) to lease agreement.

Enquire as to whether any gain is expected to be made on the sale of assets, and ensure that if so, the gain has

not been taken into account when measuring the provision.

Tutorial note: HKAS 37 prescribes that only costs necessarily entailed by the restructuring and not associated with

the ongoing activities of the business may be included in the provision. In practice this means that very few costs

can be included, and costs to do with relocation of employees, plant and equipment and inventories, retraining

staff, investments in new infrastructure are not included as they are related to ongoing activities.

Review the relevant disclosure note to the financial statements for accuracy and adequacy, where the provision

should be treated as a separate numerical class and a description of it given.

Tutorial note: Credit will also be awarded for procedures relevant to ascertaining whether the factory closure

constitutes a discontinued operation, and procedures relevant to any consequential disclosure requirements.

(ii) Measuring and reporting on social and environmental performance

Many companies attempt to measure social and environmental performance by setting targets or key performance

indicators (KPIs), and then evaluating whether they have been met. The results are often published to enable a

comparison to be made year on year or between companies. But it can be difficult to measure social and environmental

performance for a number of reasons.

First, targets and KPIs are not always precisely defined. For example, Osprey Co may state a target of reducing

environmental damage caused by its operations, but this is very vague. It is difficult to measure and compare

performance unless a target or KPI is made more specific, for example, a target of reducing electricity consumption by

5% per annum.

Second, targets and KPIs may be difficult or impossible to quantify, with Osprey Co’s planned KPI on employee

satisfaction being a good example. This is a very subjective matter, and while there are methods that can be used to

gauge the levels of employee satisfaction, whether this can result in a meaningful statistic is questionable.

Third, systems and controls are often not established well enough to allow accurate measurement, and the measurement

of socio-environmental matters may not be based on reliable evidence. In Osprey Co’s case, it may not be possible to

quantify how much toxic chemical has been leaked from the factory.

Finally, it is hard to compare these targets and KPIs between companies, as they are not strictly defined, so each

company will set its own target. It will also be difficult to make year on year comparisons for the same company, as

targets may change in response to business activities. For example, if Osprey Co were to expand its operating, its energy

and water use would increase, making its performance on environmental matters look worse. Users would need to

understand the context in order to properly appraise why a target had not been met.

Conclusion

These briefing notes have shown that the environmental incident at Osprey Co will have an impact on our audit in that

detailed audit procedures will need to be conducted to gain evidence regarding whether or not a provision for costs of closure

should be recognised, and if so, its measurement. In addition, Osprey Co’s intention to publish socio-environmental targets

and KPIs is commendable, but it will be difficult for management to measure and report on these matters due to their often

subjective nature.20

3 (a) (i) The circumstances described by the audit senior indicate that Jack Heron may be using his company to carry out money

laundering. Money laundering is defined as the process by which criminals attempt to conceal the origin and ownership

of the proceeds of their criminal activity, allowing them to maintain control over the proceeds and, ultimately, providing

a legitimate cover for the sources of their income. Money laundering activity may range from a single act, such as being

in possession of the proceeds of one’s own crime, to complex and sophisticated schemes involving multiple parties, and

multiple methods of handling and transferring criminal property as well as concealing it and entering into arrangements

to assist others to do so.

Heron Co’s business is cash-based, making it an ideal environment for cash acquired through illegal activities to be

legitimised by adding it to the cash paid genuinely by customers and posting it through the accounts. It appears that

$2 million additional cash has been added to the genuine cash receipts from customers. This introduction of cash

acquired through illegal activities into the business is known as ‘placement’.

The fact that the owner himself posts transactions relating to revenue and cash is strange and therefore raises suspicions

as to the legitimacy of the transactions he is posting through the accounts. Suspicions are heightened due to Jack

Heron’s refusal to explain the nature and reason for the journal entries he is making in the accounts.

The $2 million paid by electronic transfer is the same amount as the additional cash posted through the accounts. This

indicates that the cash is being laundered and the transfer is known as the ‘layering’ stage, which is done to disguise

the source and ownership of the funds by creating complex layers of transactions. Money launderers often move cash

overseas as quickly as possible in order to distance the cash from its original source, and to make tracing the transaction

more difficult. The ‘integration’ stage of money laundering occurs when upon successful completion of the layering

process, the laundered cash is reintroduced into the financial system, for example, as payment for services rendered.

The secrecy over the reason for the cash transfer and lack of any supporting documentation is another indicator that this

is a suspicious transaction.

Jack Heron’s reaction to being questioned over the source of the cash and the electronic transfer point to the fact that

he has something to hide. His behaviour is certainly lacking in integrity, and even if there is a genuine reason for the

journals and electronic transfer his unhelpful and aggressive attitude may cast doubts as to whether the audit firm wish

to continue to retain Heron Co as a client.

The audit senior was correct to be alarmed by the situation. However, by questioning Jack Heron about it, the senior

may have alerted him to the fact that the audit team is suspicious that money laundering is taking place. There is a

potential risk that the senior has tipped off the client, which may prejudice any investigation into the situation.

Tipping off is itself an offence, though this can be defended against if the person did not know or suspect that the

disclosure was likely to prejudice any investigation that followed.

The amount involved is clearly highly material to the financial statements and will therefore have an implication for the

audit. The whole engagement should be approached as high risk and with a high degree of professional skepticism.

The firm may wish to consider whether it is appropriate to withdraw from the engagement (if this is possible under

applicable law and regulation). However, this could result in a tipping off offence being committed, as on withdrawal

the reasons should be discussed with those charged with governance.

If Lark & Co continue to act as auditor, the audit opinion must be considered very carefully and the whole audit subject

to second partner review, as the firm faces increased liability exposure. Legal advice should be sought.

Tutorial note: Credit will also be awarded for discussion of other relevant matters, such as fraud, internal control

deficiencies and audit implications.

(ii) The audit senior should report the situation in an internal report to Lark & Co’s Money Laundering Reporting Officer

(MLRO). The MLRO is a nominated officer who is responsible for receiving and evaluating reports of suspected money

laundering from colleagues within the firm, and making a decision as to whether further enquiries are required and if

necessary making reports to the appropriate external body.

Lark & Co will probably have a standard form that should be used to report suspicions of money laundering to the MLRO.

Tutorial note: According to ACCA’s Technical Factsheet 145 Anti-Money Laundering Guidance for the Accountancy

Sector, there are no external requirements for the format of an internal report and the report can be made verbally or

in writing.

The typical content of an internal report on suspected money laundering may include the name of the suspect, the

amounts potentially involved, and the reasons for the suspicions with supporting evidence if possible, and the

whereabouts of the laundered cash.

The report must be done as soon as possible, as failure to report suspicions of money laundering to the MLRO as soon

as practicable can itself be an offence under the money laundering regulations.

The audit senior may wish to discuss their concerns with the audit manager in more detail before making the report,

especially if the senior is relatively inexperienced and wants to hear a more senior auditor’s view on the matter. However,

the senior is responsible for reporting the suspicious circumstances at Heron Co to the MLRO.

Tutorial note: ACCA’s Technical Factsheet 145 states that: ‘An individual may discuss his suspicion with managers or

other colleagues to assure himself of the reasonableness of his conclusions but, other than in group reporting

circumstances, the responsibility for reporting to the MLRO remains with him. It cannot be transferred to anyone else,

however junior or senior they are.’21

(b) The term professional skepticism is defined in HKSA 200 Overall Objectives of the Independent Auditor and the Conduct of

an Audit in Accordance with HKSAs as follows: ‘An attitude that includes a questioning mind, being alert to conditions which

may indicate possible misstatement due to error or fraud, and a critical assessment of audit evidence’.

Professional skepticism means for example, being alert to contradictory or unreliable audit evidence, and conditions that may

indicate the existence of fraud. If professional skepticism is not maintained, the auditor may overlook unusual circumstances,

use unsuitable audit procedures, or reach inappropriate conclusions when evaluating the results of audit work. In summary,

maintaining an attitude of professional skepticism is important in reducing audit risk.

IFAC’s Code of Ethics for Professional Accountants also refers to professional skepticism when discussing the importance of

the auditor’s independence of mind. It can therefore be seen as an ethical as well as a professional issue.

In the case of the audit of Coot Co, the audit junior has not exercised a sufficient degree of professional skepticism when

obtaining audit evidence. Firstly, the reliability of the payroll supervisor’s response to the junior’s enquiry should be

questioned. Additional and corroborating evidence should be sought for the assertion that the new employees are indeed

temporary.

The absence of authorisation should also be further investigated. Authorisation is a control that should be in place for any

additions to payroll, so it seems unusual that the control would not be in place even for temporary members of staff.

If it is proved correct that no authorisation is required for temporary employees the audit junior should have identified this as

a control deficiency and made a management letter point to be reported to those charged with governance.

The contradictory evidence from comments made by management also should be explored further. HKSA 500 Audit Evidence

states that ‘if audit evidence obtained from one source is inconsistent with that obtained from another... the auditor shall

determine what modifications or additions to audit procedures are necessary to resolve the matter’.

Additional procedures should therefore be carried out to determine which source of evidence is reliable. Further discussions

should be held with management to clarify whether any additional employees have been recruited during the year.

The amendment of payroll could indicate that a fraud (‘ghost employee’) is being carried out by the payroll supervisor.

Additional procedures should be conducted to determine whether the supervisor has made any other amendments to payroll

to determine the possible scope of any fraud. Verification should be sought as to the existence of the new employees. The

bank accounts into which their salaries are being paid should also be examined, to see if the payments are being made into

the same account.

Finally, the audit junior should be made aware that it is not acceptable to just put a note on the file when matters such as

the lack of authorisation come to light during the course of the audit. The audit junior should have discussed their findings

with the audit senior or manager to seek guidance and proper supervision on whether further testing should be carried out.

4 (a) The business venture proposed by Grouse Co’s managing director, while potentially lucrative for the audit firm, would create

significant threats to objectivity. A financial interest in a joint venture such as the one being proposed is an example of a close

business arrangement given in IFAC’s Code of Ethics for Professional Accountants.

According to the Code, a close business relationship between an audit firm and the audit client or its management, which

arises from a commercial relationship or common financial interest, may create self-interest or intimidation threats. The audit

firm must maintain independence, and the perception of independence will be affected where the audit firm and client are

seen to be working together for mutual financial gain.

Unless the financial interest is immaterial and the business relationship is insignificant to the firm and the client or its

management, the threat created by the joint venture would be so significant that no safeguards could reduce the threat to

objectivity to an acceptable level. Therefore, unless the financial interest is immaterial and the business relationship is

insignificant, the business relationship should not be entered into.

There would also be ethical issues raised if Raven & Co were to sell the software packages to audit clients. First, there would

be a self-interest threat, as the audit firm would benefit financially from the revenues generated from such sales. Full

disclosure would have to be made to clients in order for them to be made aware of the financial benefit that Raven & Co

would receive on the sale.

Second, there would be a self-review threat, as when performing the audit, the audit team would be evaluating the accounting

software which itself had sold to the audit client, and auditing tax figures generated by the software. It is difficult to see how

this threat could be reduced to an acceptable level as the accounting and tax software would be fundamental to the

preparation of the financial statements.

Third, by recommending the software to audit clients, it could be perceived that the audit firm is providing a non-audit service

by being involved with tax calculations, and providing IT systems services. The provision of non-audit services creates several

threats to objectivity, including a perception of taking on management’s responsibilities. Risks are heightened for audit clients

that are public interest entities, for example, the audit firm should not be involved with tax calculations for such clients

according to IFAC’s Code.

If having considered the ethical threats discussed above, Raven & Co still wishes to pursue the business arrangement, they

must cease to act as Grouse Co’s auditors with immediate effect. The lost income from the audit fee of Grouse Co should also

be taken into account, as it is a ‘significant’ client of the firm.22

The potential commercial benefits of the business venture should be considered carefully, as there may be little demand for

the suggested product, especially as many software packages of this type are already on the market. Also, the quality of the

software developed should be looked into, as if Raven & Co recommends inferior products they will lose customers and could

face bad publicity.

Finally, if Raven & Co decides to go ahead with the joint venture, the partners would need to consider if such a diversification

away from the firm’s core activity would be advisable. The partners may have little experience in such a business, and it may

be better for the firm to concentrate on providing audit and assurance services.

(b) It appears that a surgeon is carrying out medical procedures without the necessary qualifications. This could clearly lead to

serious damage being caused to a patient while undergoing laser eye surgery, and indeed this seems to have already occurred.

The medical profession is highly regulated, and it is important for the auditor to consider obligations in the event of any serious

breach of laws and regulations relevant to Plover Co.

It is management’s responsibility that laws and regulations are followed, and auditors are not expected to prevent or detect

non-compliance, especially non-compliances which have limited impact on the financial statements.

HKSA 250 Consideration of Laws and Regulations in an Audit of Financial Statements provides relevant guidance. It is

required that if the auditor becomes aware of a suspected non-compliance, an understanding of the nature of the act and the

circumstances in which it occurred should be obtained.

Therefore the auditor should establish whether it is the case that the surgeon is not qualified, possibly through reviewing the

personnel file of the surgeon or discussing with the person responsible for recruitment.

The auditor should also discuss the matter with management and/or those charged with governance. It may be that they are

unaware of the surgeon’s apparent lack of qualifications, or possibly there is an alternative explanation in that the surgeon is

qualified to perform laser eye surgery but does not possess a full medical qualification.

The potential impact of the apparent non-compliance should be evaluated. In this case, Plover Co could face further legal

action from dissatisfied or injured patients, fines and penalties from the regulatory authorities and its going concern may be

in jeopardy if that authority has the power to revoke its operating licence. If these potential effects are considered to be material

to the financial statements, legal advice may need to be obtained.

In the event that the surgeon’s work is in breach of relevant laws and regulations, management should be encouraged to

report the non-compliance to the relevant authority.

If management fail to make such a disclosure, the auditor should consider making the necessary disclosure. However, due

to the professional duty to maintain the confidentiality of client information, it is generally not acceptable to disclose

client-related matters to external parties.

ACCA’s Code of Ethics and Conduct provides additional guidance, stating that a member may disclose information which

would otherwise be confidential if disclosure can be justified in the public interest. There is no definition of public interest

which places members in a difficult position as to whether or not disclosure is justified. Matters such as the gravity of the

situation, whether members of the public may be affected, and the possibility and likelihood of repeated non-compliance

should be considered.

Determination of where the balance of public interest lies will require very careful consideration and it will often be appropriate

to take legal advice before making a decision. The reasons underlying any decision whether or not to disclose should be fully

documented.

The fact that a legal claim has been filed against Plover Co means that the audit work on provisions and contingent liabilities

should be extended. Further evidence should be obtained regarding the legal correspondence, in particular the amount of the

compensation claim. The date of the claim and the date of the medical incident to which it relates should also be ascertained

in order to determine whether a provision for the claim should be recognised in accordance with HKAS 37 Provisions,

Contingent Liabilities and Contingent Assets, or whether a note to the financial statements regarding the non-adjusting event

should be made.

Tutorial note: Per HKAS 37 commencing major litigation arising solely out of events that occurred after the year end is an

example of a non-adjusting event after the reporting period.

The audit firm may wish to consider the integrity of the audit client. If the management of Plover Co knowingly allowed an

unqualified person to carry out medical procedures then its integrity is questionable, in which case Raven & Co may wish to

resign from the audit appointment as soon as possible. This is especially important given the legal claim recently filed against

the client, which could result in bad publicity for Plover Co, and possibly by association for Raven & Co.

5 (a) Matters to consider

The total cost of the new processing area of $5 million represents 29% of total assets and is material to the statement of

financial position. The borrowing costs are not material to the statement of financial position, representing less than 1% of

total assets; however, the costs are material to profit representing 10% of profit before tax.

The directly attributable costs, including borrowing costs, relating to the new processing area should be capitalised as

property, plant and equipment. According to HKAS 23 Borrowing Costs, borrowing costs that are directly attributable to the23

acquisition, construction or production of a qualifying asset should be capitalised as part of the cost of that asset. The

borrowing costs should be capitalised only during the period of construction, with capitalisation ceasing when substantially

all the activities necessary to prepare the qualifying asset for its intended use or sale are complete.

In this case, the new processing area was ready for use on 1 September, so capitalisation of borrowing costs should have

ceased at that point. It seems that the borrowing costs have been appropriately capitalised at $100,000, which represents

six months’ interest on the loan ($4m x 5% x 6/12).

The new processing area should be depreciated from 1 September, as according to HKAS 16 Property, Plant and Equipment,

depreciation of an asset begins when it is in the location and condition necessary for it to be capable of operating in the

manner intended by management.

There should therefore be five months’ depreciation included in profit for the year ended 31 January 2012, amounting to

$138,889 ($5m/15 years x 5/12).

Evidence

A breakdown of the components of the $49 million capitalised costs (excluding $100,000 borrowing costs) reviewed

to ensure all items are eligible for capitalisation.

Agreement of a sample of the capitalised costs to supporting documentation (e.g. invoices for tangible items such as

cement, payroll records for internal labour costs).

A copy of the approved budget or capital expenditure plan for the extension.

An original copy of the loan agreement, confirming the amount borrowed, the date of the cash receipt, the interest rate

and whether the loan is secured on any assets.

Documentation to verify that the extension was complete and ready for use on 1 September, such as a building

completion certificate.

Recalculation of the borrowing cost, depreciation charge and carrying value of the extension at the year end, and

agreement of all figures to the draft financial statements.

Confirmation that the additions to property, plant and equipment are disclosed in the required note to the financial

statements.

(b) The titles and positioning of the two paragraphs included in the extract are not appropriate. According to HKSA 705

Modifications to the Opinion in the Independent Auditor’s Report, when the auditor modifies the opinion, a paragraph should

be placed immediately before the opinion paragraph entitled ‘Basis for Adverse Opinion’, which describes the matter giving

rise to the modification. This should then be followed by the opinion paragraph, which should be entitled ‘Adverse Opinion’.

In this case, the titles are incorrect, and the paragraphs should be switched round, so that the basis for modification is

provided before the opinion.

The description and explanation provided for the adverse opinion is not sufficient, for a number of reasons. Firstly, the matter

is not quantified. The paragraph should clearly state the amount of $105 million, and state that this is material to the

financial statements.

The paragraph does not say whether the pension plan is in surplus or deficit, i.e. whether it is an asset or a liability which is

omitted from the financial statements.

There is no description of the impact of this omission on the financial statements. Wording such as ‘if the deficit had been

recognised, total liabilities would increase by $105 million, and shareholders’ equity would reduce by the same amount’

should be included.

It is not clear whether any accounting for the pension plan has taken place at all. As well as recognising the plan surplus or

deficit in the statement of financial position, accounting entries are also required to deal with other items such as the current

service cost of the plan, and any actuarial gains or losses which have arisen during the year. Whether these have been omitted

as well, and their potential impact on profit or equity is not mentioned.

No reference is made to the relevant accounting standard HKAS 19 Employee Benefits. Reference should be made in order

to help users’ understanding of the breach of accounting standards that has been made.

The use of the word ‘deliberate’ when describing the omission of the pension plan is not professional, sounds accusatory and

may not be correct. The plan may have been omitted in error and an adjustment to the financial statements may have been

suggested by the audit firm and is being considered by management.

Finally, it is unlikely that this issue alone would be sufficient to give rise to an adverse opinion. HKSA 705 states that an

adverse opinion should be given when misstatements are both material and pervasive to the financial statements. The amount

of the deficit, and therefore the liability that should be recognised, is $105 million, which represents 6% of total assets. The

amount is definitely material, but would not be considered pervasive to the financial statements.

Tutorial note: According to HKSA 705 if a misstatement is confined to specific elements of the financial statements, it would

only be considered pervasive if it represents a substantial proportion of the financial statements.25

Professional Level Options Module, Paper P7 (HKG)

Advanced Audit and Assurance (Hong Kong) June 2012 Marking Scheme

Marks

1 (a) (i) Audit implications of Canary Co acquisition

Up to 1½ marks for each implication explained (3 marks maximum for identification):

Develop understanding of Canary Co business environment

Document Canary Co accounting systems and controls

Perform detailed analytical procedures on Canary Co

Communicate with previous auditor

Review prior year audit opinion for relevant matters

Plan additional work on opening balances

Determine that Canary Co is a significant component of the Group

Plan for audit of intra-company transactions

Issues on auditing the one month difference in financial year ends

Impact of acquisition on analytical procedures at Group level

Additional experienced staff may be needed, e.g. to audit complex goodwill

Maximum marks 8

(ii) Risk of material misstatement

Up to 1½ marks for each risk (unless a different maximum is indicated below):

General risks diversification, change to group structure

Goodwill contingent consideration estimation uncertainty (probability of payment)

Goodwill contingent consideration measurement uncertainty (discounting)

Goodwill fair value of net assets acquired

Goodwill impairment

Identify that the issues in relation to cost of investment apply also in Crow Co’s

individual financial statements (1 mark)

Loan stock premium on redemption

Loan stock accrued interest

Loan stock inadequate disclosure

Identify that the issues in relation to loan stock apply to cost of investment in Crow Co’s

individual financial statements (1 mark)

Online sales and risk relating to revenue recognition (additional 1 mark if calculation

provided of online sales materiality to the Group)

No group accounting policy for online sales

Canary Co management have no experience regarding consolidation

Financial performance of Crow Co and Starling Co deteriorating (up to 3 marks with calculations)

Possible misstatement of Canary Co revenue and profit

Grant received capital expenditure

Grant received amount not yet spent

New IT system

Starling Co no finance director in place at year end

Maximum marks 18

(iii) Goodwill

Generally 1 mark per specific procedure (examples shown below):

Confirm acquisition date to legal documentation

Confirm consideration details to legal documentation

Agree 100% ownership, e.g. using Companies House search/register of significant shareholdings

Vouch consideration paid to bank statements/cash book

Review board minutes for discussion/approval of acquisition

Obtain due diligence report and agree net assets valuation

Discuss probability of paying contingent consideration

Obtain management representation regarding contingency

Recalculate goodwill including contingency on a discounted basis

Maximum marks 5Marks

(b) Ethical matters

Generally 1 mark per comment:

Reasonable for partner to attend board meetings

But must avoid perception of management involvement

Partner must not be appointed to the board

Seconded manager would cause management and self-review threat

Safeguards could not reduce these threats to an acceptable level

Some recruitment services may be provided interviewing/CV selection

But avoid making management decision and put safeguards in place

Maximum marks 6

Maximum 37

26Marks

2 (a) (i) Matters to be considered in agreeing the terms of the engagement

Up to 1½ marks for each matter identified and explained (2 marks maximum for identification):

Management’s responsibilities

Intended use of the information and report

The contents of the business plan

The period covered by the forecasts

The nature of assumptions used in the forecasts

The format and planned content of the assurance report

Maximum marks 6

(ii) Procedures on forecast financial information

Up to 1 mark for each procedure (brief examples below):

General procedures examples:

o Re-perform calculations

o Consistency of accounting policies used

o Discuss how joint venture has been included

o General analytical procedures

Procedures on income statement:

o Discuss trends allow up to 3 marks for calculations performed and linked to procedures

o Review and compare breakdown of costs

o Recalculate profit on disposal, agreement of components to supporting documentation

Procedures on statement of financial position:

o Agree increase in property, plant and equipment to capital expenditure budget

o Discuss working capital trends allow 2 marks for calculations performed and linked to

procedures

o Agree movement in long-term borrowings to new loan documentation

o Obtain and review forecast statement of changes in equity and confirm validity of

reconciling items

Maximum marks 13

(b) (i) Audit procedures on costs of closure

Generally 1 mark per specific procedure, examples given below:

Review board minutes for discussion and date of decision

Review detailed, formal plan and date of its approval

Review any public announcement and the date it was made

Physically inspect factory prior to year end for evidence of dismantling of assets

Consider whether costs included are relevant (redundancies and lease cancellation fees are

the most common type of relevant costs included)

Agree relevant costs to supporting documentation

Review note to financial statements for accuracy and completeness

Maximum marks 6

(ii) Problems in measuring and reporting on social and environmental performance

Up to 1½ marks per comment discussed:

Difficulties in defining and measuring targets and KPIs

Problems in quantifying some measures, e.g. employee satisfaction

Inadequate systems and controls to accurately measure

Difficult to compare between companies or over time

Maximum marks 4

Professional marks for the overall presentation of the notes, and the clarity of the explanation and

assessment provided.

Maximum marks 4

Maximum 33

27Marks

3 (a) (i) Implications of the audit senior’s note

Generally 1 mark for each matter discussed relevant to money laundering:

Definition of money laundering

Placement cash-based business

Owner posting transactions

Layering electronic transfer to overseas

Secrecy and aggressive attitude

Audit to be considered very high risk

Senior may have tipped off the client

Firm may consider withdrawal from audit

But this may have tipping off consequences

Maximum marks 6

(ii) Reporting that should take place

Generally 1 mark for each comment:

Report suspicions immediately to MLRO

Failure to report is itself an offence

Examples of matters to be reported (identity of suspect, etc)

Audit senior may discuss matters with audit manager but senior responsible for the report

Maximum marks 3

(b) Professional skepticism

Generally 1 mark for each comment:

Definition of professional skepticism

Explain alert to contradictory evidence/unusual events/fraud indicator (up to 2 marks)

Part of ethical codes

Coot Co evidence is unreliable and contradictory

Absence of authorisation is fraud indicator

Additional substantive procedures needed

Management’s comments should be corroborated

Control deficiency to be reported to management/those charged with governance

Audit junior needs better supervision/training on how to deal with deficiencies identified

Maximum marks 6

Maximum 15

28Marks

4 For each requirement, generally 1 mark for each matter discussed:

(a) Grouse Co

Situation is a close business arrangement giving rise to threat to objectivity

Explain self-interest threat

Explain intimidation threat

Only acceptable if financial interest immaterial and relationship insignificant

Sale of software to audit clients would require full disclosure of financial benefit

Sale of software to audit clients creates self-review threat

Sale of software perceived as providing non-audit service

Risks heightened for listed/public interest entities

If enter business arrangement must withdraw from audit of Grouse Co

Commercial consideration demand for product

Commercial consideration experience of partners

Maximum marks 8

(b) Plover Co

Potential breach of law and regulations

Further understanding to be obtained

Consider potential impact on financial statements

Discuss with those charged with governance

Management should disclose to relevant regulatory body

Auditor could disclose in public interest

Issues with confidentiality

Take legal advice

Extend audit work in relation to the legal claim

Risk of material misstatement

Consider integrity of audit client

Maximum marks 7

Maximum 15

29Marks

5 (a) New processing area

Generally 1 mark for each matter/specific audit procedure:

Matters:

Materiality calculation

Borrowing costs are directly attributable to the asset

Borrowing costs should be capitalised during period of construction

Amounts are correctly capitalised

Depreciate from September 2011

Additions to non-current assets should be disclosed in note

Evidence:

Review of costs capitalised for eligibility

Agreement of sample of costs to supporting documentation

Copy of approved capital expenditure budget/discuss significant variances

Agreement of loan details to loan documentation

Recalculation of borrowing costs, depreciation, asset carrying value

Confirmation of completeness of disclosure in notes to financial statements

Maximum marks 8

(b) Audit report

Generally 1 mark per comment:

Inappropriate headings

Paragraphs wrong way round

Amounts not quantified

Impact on financial statements not described

Unclear from audit report if any accounting taken place for the pension plan

No reference made to relevant accounting standard

Use of word ‘deliberate’ not professional

Materiality calculation

Discuss whether adverse opinion appropriate (up to 2 marks)

Maximum marks 7

Maximum 15

相关推荐:

ACCA教材辅导讲义——Pilotpapers for F3

更多ACCA考试信息请关注读书人网(http://www.reader8.net/)

ACCA频道(http://www.reader8.net/exam/acca/)